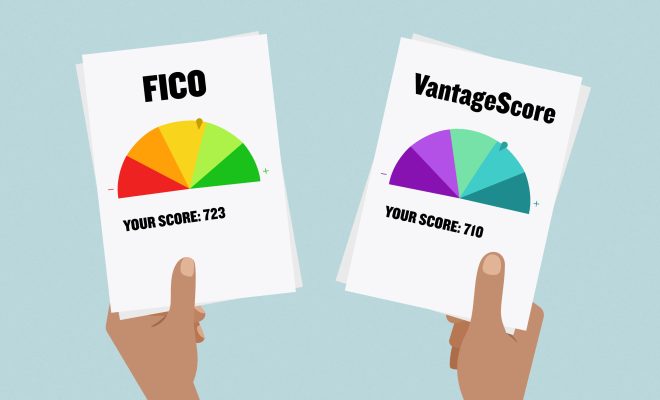

FICO Vs. VantageScore Credit Scores: What’s The Difference?

When it comes to credit scores, two scoring models stand out: FICO and VantageScore. These two models have established themselves as the leading credit score providers in the industry. Although they share some similarities, there are also key differences between FICO and VantageScore. In this article, we will explore the distinctions between these two credit scoring models to help you better understand their impact on your financial health.

FICO Credit Score

Developed by Fair Isaac Corporation, FICO credit scores are among the most widely used credit scoring models. FICO scores range from 300 to 850, with higher scores indicating a more favorable creditworthy profile. These scores are crucial in determining lending decisions for mortgages, car loans, and credit cards.

FICO scores are calculated using five main factors:

1. Payment history (35%): Your record of timely (or late) payments

2. Amounts owed (30%): Cumulative debt across all lines of credit

3. Length of credit history (15%): The age of your oldest and newest accounts

4. Credit mix (10%): Diversity of credit types in your portfolio

5. New credit inquiries (10%): Recent applications for additional credit

VantageScore Credit Score

Launched in 2006 by the three major credit bureaus (Experian, TransUnion, and Equifax), VantageScore was developed as an alternative to FICO scores. Similar to FICO, VantageScore ranges from 300 to 850.

VantageScore uses a different calculation methodology than FICO:

1. Payment history (40%): The most crucial factor for VantageScore as well

2. Age and type of credit (21%): A combination of the age of your accounts and the diversity in your portfolio

3. Credit utilization (20%): The percentage of your available credit in use

4. Total balances and debt (11%): The amount you owe across all accounts

5. Recent credit behavior and inquiries (5%): Applications for new credit and recent account activity

6. Available credit (3%): The total unused credit open to you

Key Differences between FICO and VantageScore

1. Scoring model: While both FICO and VantageScore use the same range of 300 to 850, their calculation methodologies are different, resulting in varying score outcomes.

2. Treatment of late payments: FICO is more lenient towards single late payments, while VantageScore penalizes borrowers more severely for such infractions.

3. Credit history: VantageScore can generate scores for individuals with limited or no credit history by considering non-traditional factors like rent and utility payments.

4. Inquiries: FICO divides inquiries into separate categories for mortgage, auto, and student loans, while VantageScore treats all inquiries alike.

In conclusion, though both FICO and VantageScore credit scores share core similarities, there exist significant differences in their scoring methodologies that can influence your overall financial standing. Understanding these distinctions can help you make better decisions when managing your credit health.